Article Directory

So, the headlines are whispering sweet nothings in your ear again. "Mortgage Rates Dip!" they scream, like it's the second coming. The 30-year fixed rate dropped a whole tenth of a percent to 6.19%. Break out the champagne, right?

Give me a break.

Celebrating this is like being happy your fever dropped from 103 to 102.8. You’re still sick. The house is still on fire. We're living through a government shutdown so prolonged that the agency in charge of telling us how many people are unemployed... can't. They're shut down. The irony is so thick you could cut it with a knife.

And in the middle of this self-inflicted paralysis, we're supposed to get excited about a microscopic dip in borrowing costs? This isn't a sign of a healthy market. It's a symptom of a deeply diseased one.

The "Flight to Safety" Charade

Some guy from a mortgage company, Derek Egeberg, called this a "flight to safety." Let's translate that from corporate-speak into plain English. A "flight to safety" is when people with money get so terrified by the chaos they helped create that they pull their cash out of anything that looks risky and dump it into boring, reliable government bonds. This flood of scared money into bonds pushes bond yields down, and mortgage rates tend to follow.

So, this rate dip isn't a gift. It's a distress signal. It's the financial equivalent of lifeboats being lowered from the Titanic. The people in first class are patting themselves on the back for securing a spot, while the rest of us are just trying to figure out where the hell all this water is coming from. Are we really supposed to cheer because the architects of this mess are now running for cover?

This isn't a calculated market correction. It's a panic attack. And they're trying to sell it to you as a discount. It's a bad joke. No, 'bad' doesn't cover it—this is a five-alarm dumpster fire of economic messaging. We have no official employment data. The Federal Reserve is about to meet and probably spin some new fairytale about "transitory" problems. And the CPI inflation report is due out any second now, which will almost certainly tell us that everything we need to live is more expensive. But hey, at least your hypothetical mortgage is 0.10% cheaper this week. What a steal.

Let's Talk About the Real Numbers

The spin doctors want you to focus on the week-over-week change. Look at the shiny object! Don't look at the bigger picture. Because the bigger picture is ugly.

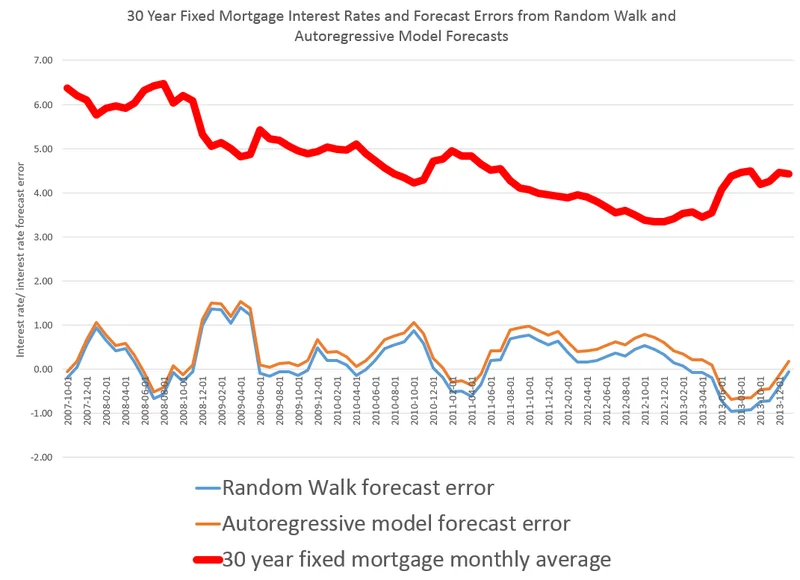

The average 30-year rate for 2025 has been 6.81%. So, at 6.19%—a number confirmed by reports like 30-year mortgage rates fall - When should you lock? | Today's mortgage and refinance rates, October 24, 2025 - Bankrate—we're still well below the year's average, but let's not pretend this is some historic opportunity. The 40-year average is 7.2%. We've been so conditioned by a decade of near-zero interest rates that we've forgotten what "normal" even looks like. This ain't it.

This whole situation reminds me of those old cartoons where a character runs off a cliff and keeps running on thin air, only falling when he finally looks down. That's our economy. We're running on fumes, tariffs, and political gridlock, and the only reason the whole thing hasn't plunged into the canyon is because the official statisticians who are supposed to tell us we're falling have all been sent home. The goverment can't even perform its most basic functions, and we're supposed to make 30-year financial commitments based on this circus?

And what happens next week, when the Fed meets? They're trapped. If they cut rates again, they signal that they're panicking. If they hold steady, they risk choking off what little oxygen is left in the economy. They'll probably come out and say something completely meaningless about "monitoring the data," and the market will pretend to understand what that means, and the whole charade will continue for another month. Honestly, it's just...

What's the real game here? Is this managed chaos designed to let the big players reshuffle their decks while the rest of us get wiped out? Or is it genuine, top-to-bottom incompetence? I'm not sure which is worse.

This Is Just Noise

Look, a tenth of a point is a rounding error in the grand scheme of things. Don't let it distract you. The fundamental questions remain unanswered. When will the government reopen? What will the next inflation print look like? How long can we pretend that everything is fine when the foundational data we use to measure "fine" isn't even being collected?

This small dip in mortgage rates isn't a sign of recovery. It's a flicker in the matrix, a piece of static in a broadcast filled with lies. Don't fall for it. The real storm hasn't even hit yet.